Beyond the Soloist

When 500 stocks start behaving like one trade

If today’s SpaceX IPO tells us anything, it’s that markets have drifted a long way from everything conventional investing wisdom told us to expect. Some are sounding the alarm, but the market isn’t listening yet. Meanwhile, the warning lights are coming on one at a time, and they’re worth reading in sequence.

The first light flickers on at the index providers themselves. A single new listing was enough to send the committees that govern the world’s major benchmarks into an identity crisis. Nasdaq rewrote its rules to admit mega-cap IPOs in just 15 trading days, down from a three-month minimum, and FTSE Russell cut its wait to five, while S&P Dow Jones Indices rejected its own proposal to relax the criteria, keeping SpaceX out of the S&P 500 until at least mid-2027. When one company’s debut forces the gatekeepers to debate, and in some cases rewrite, what justifies inclusion at all, something fundamental is shifting.

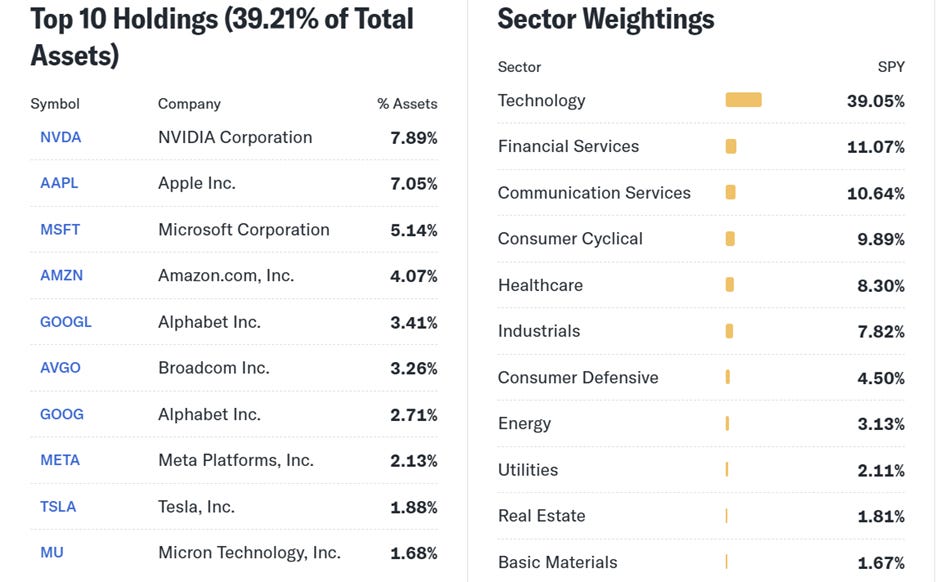

The second light is concentration. The ten largest companies in the S&P 500 now account for just over 39% of the index. The benchmark sold to investors as instant diversification has quietly become a concentrated bet on a handful of names.

The third light is the one investors sometimes forget to check: the labels. Technology, as a sector, accounts for another 39% of the index. That those two numbers match is no coincidence, they’re largely the same names. And even that figure understates things: Amazon is classified as a Consumer company, never mind that AWS is the profit engine of the whole enterprise. Tesla carries the same label, despite Elon Musk’s standing argument that autonomous driving and EV leadership make it a technology company first. The clear conclusion: the index’s true tech exposure runs well past what the official sector weights admit, and the official number already looked excessively concentrated.

One light is a glitch. Two is a coincidence. Three, and the whole panel is blaring, and at that point, the right response isn’t to keep travelling along the same route and hope for the best. It’s to ask whether the route still makes sense at all.

Take Me Back

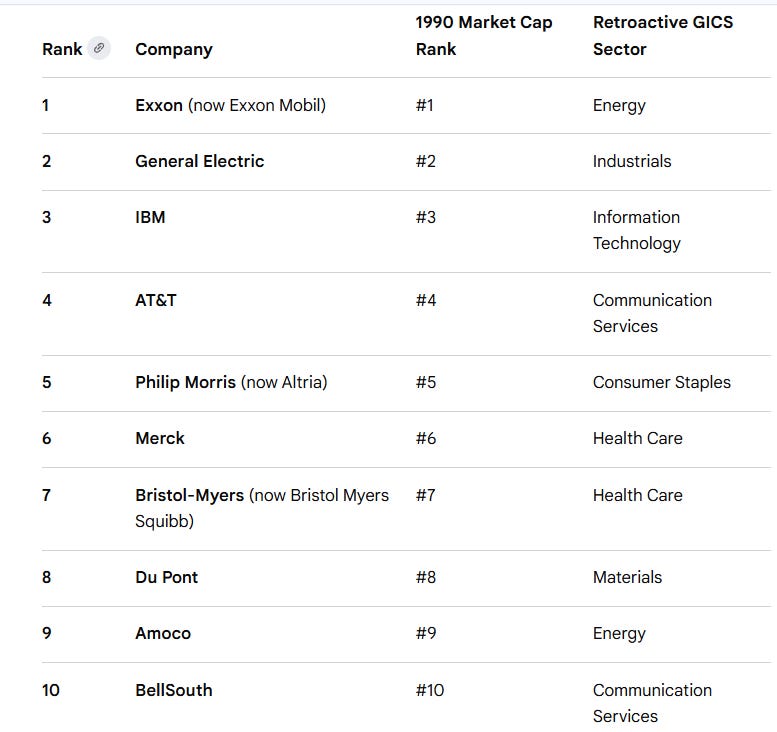

In the early 90s, the S&P 500 looked like a far more representative cross-section of the U.S. economy. The 10 largest companies by market cap (IBM, Exxon, General Electric and Philip Morris, etc.) made up roughly 19% of the index. Leadership was spread across multiple sectors, and no single industry dominated overall returns.

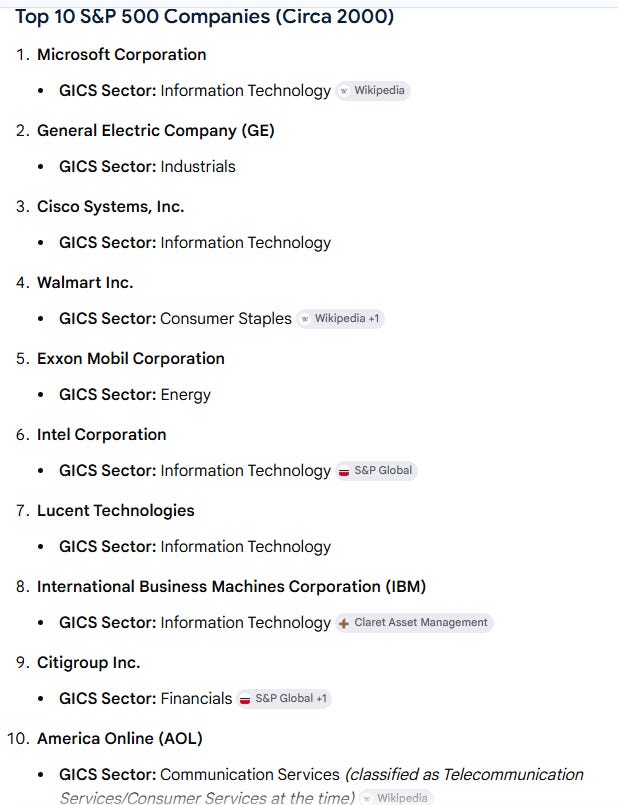

That began to change during the technology boom. By the end of 2000, the top 10 accounted for roughly 23% of the index, with concentration peaking during the year at about 27%, driven by the rise of companies such as Cisco, Microsoft and Intel. As we aspiring market historians know, the subsequent unwind was sharp, and the early-2000s reset ushered in a period where concentration declined as energy and consumer stocks came back to dominate.

But before we leave the 90s entirely, sit with that fact for a moment: 27%. At the height of the dot-com era, the time period every market watcher uses as the cautionary tale, the top 10 commanded barely two-thirds of the weight they hold today. The balance has shifted dramatically in just the past decade: today’s 39% is roughly double where the top 10 stood ten years ago. And the weight has run ahead of the earnings. In 2025, the top 10 stocks represented roughly 41% of the index’s total weight but were expected to generate only about 32% of its earnings, a gap that has widened meaningfully since 2015, when weight and earnings contribution were closely aligned. The largest companies remain highly profitable, but market value concentration has increasingly outpaced fundamental profitability.

Concentration risk is at an all-time high. Correlations are shifting in ways that expose the limits of traditional models. And simply owning more securities no longer creates a meaningfully more diversified portfolio. Many investors believe an S&P 500 fund offers wide diversification, yet roughly $39 of every $100 invested flows into just 10 companies, creating a feedback loop in which passive inflows disproportionately support the largest stocks, increasing their weights and reinforcing performance leadership regardless of fundamentals. This is also why SpaceX’s inclusion in some indices already matters so much: the moment it enters the Nasdaq-100 and Russell benchmarks, an estimated $22–27 billion in passive money must buy it, not because anyone weighed the fundamentals, but because the rules say so.

The narrowing of the S&P 500 reflects a structural shift: a handful of technology and AI-driven giants now dominate the index’s composition, performance and risk profile. The current leaders do in most cases have solid fundamentals (profitability, competitive advantages, growth trajectories) but the concentration of market value in a narrow group introduces a new kind of risk. The disconnect between weight and earnings contribution, the outsized influence of individual stocks, and passive inflows amplifying both underscore our new reality: what appears to be broad diversification increasingly functions as a concentrated allocation to a single thematic outcome.

For investors, this evolution demands a recalibration of assumptions. The index has been a resilient benchmark, but its top-heavy structure warrants a closer look. Today’s markets are not the ones we were taught in our intro to finance classes, and new markets call for new solutions.

For decades, portfolio construction felt relatively straightforward: equities provided growth, bonds provided stability, and diversification meant balancing the two. That composition played reliably for a generation. But today, investors face a more daunting question:

How do you build a portfolio capable of navigating multiple market environments without relying on a single source of return?

The answer may look less like assembling a larger portfolio and more like conducting an orchestra.

When the Music Changes

Over the past five years, a structural shift has reshaped global markets, a transition from a decade of predictable, low-cost liquidity into an environment defined by volatility, dispersion, and macro-driven uncertainty.

Persistent inflation partially eroded the safe-haven role of fixed income. Extreme market concentration rewarded a narrow set of technology names and punished everything else. And the once-reliable inverse correlation between stocks and bonds, the baseline assumption behind the 60/40 portfolio, broke down at precisely the moments investors needed it most.

In a low-rate world, the 60/40 portfolio performed as designed: equities grew the portfolio, fixed income cushioned the drawdowns. But as rates rose sharply from 2022 onward, the script flipped. Bonds fell in lockstep with equities. In some periods, fixed income became the volatility and equities provided the relative stability. The categories investors had learned to rely on began behaving like each other.

Layer onto that the concentration problem we’ve just walked through, a top 10 that commands 39% of the S&P 500, well beyond even the dot-com peak, and the picture sharpens. An investor buying a broad index fund isn’t buying the market; they’re buying a thesis, heavily weighted toward AI and large-cap technology. Add long-duration bonds to that mix, and the portfolio is doubling down on the same underlying interest-rate sensitivity, not diversifying away from it.

This is the environment liquid alternatives were built for. Multi-strategy investing has become increasingly essential precisely because it is designed to thrive on the volatility, dispersion, and macro-driven rotation that have defined the 2021–2026 period. Where traditional portfolios require calm and stable correlations to perform, a multi-strategy approach seeks to generate returns because of the turbulence … not in spite of it.

True diversification today can no longer be assembled from traditional sources alone.

More Instruments Don’t Create Better Music

Earlier, we said the answer looks less like assembling a larger portfolio and more like conducting an orchestra. Here’s what we meant.

Think about what makes a great classical performance great. You remember the melody, the emotion, the way the piece made you feel. An exceptional solo may have stood out, or a single instrument that cut through at exactly the right moment. But mostly, you sit back and let the experience wash over you. The complexity disappears into the music.

That is what well-executed multi-strategy investing feels like from the outside.

An orchestra doesn’t achieve greatness by adding more violinists. It achieves it through the deliberate combination of distinct instrument families, each with its own sound, range, and purpose. In a multi-strategy fund, the instruments are the individual funds themselves: each capable of performing independently, but most powerful when orchestrated together. The conductor reads the room (the macro environment, the market’s tempo) and makes adjustments in real time. When volatility spikes, the percussion carries. When conditions calm, the strings re-emerge.

What the portfolio manager is ultimately trying to create is a smooth listening experience. No single instrument dominates at the wrong moment. No section plays out of tune while the others hold the harmony. When one strategy isn’t performing at its expected level, the conductor shifts emphasis, bringing other sections forward until the original is ready to lead again. It is a true team effort, directed by a single, disciplined hand.

But here is the critical insight: an orchestra performs differently depending on the music.

A Beethoven symphony demands something entirely different from a piece by Vivaldi. The instruments are the same. The music hall is the same. What changes is the composition, and how each section responds to it.

Markets work the same way. The environment that rewards large-cap growth stocks may be entirely different from one that rewards small caps, real assets, or defensive strategies. Conditions rotate. Correlations shift. What worked in the last cycle may actively work against investors in the next.

Yet most portfolios are built as though the music never changes. Today, investors face a convergence of challenges that make single-strategy dependence more risky than ever:

• Extreme concentration risk in passive and large-cap equity

• Persistent uncertainty around interest rates and inflation

• Geopolitical instability with no clear resolution

• Faster and more unpredictable market rotations

The challenge isn’t predicting which movement comes next. The best conductors don’t predict, they respond. The challenge is building a portfolio capable of performing beautifully, no matter what comes next.

A quick word before we go further. The Pulse doesn’t usually do product features, but Pender built a fund around precisely the problem this piece describes, and walking through how it’s constructed is the clearest way to show what conducting an orchestra actually looks like in practice. So consider what follows equal parts illustration and disclosure: yes, it’s ours, which is also why we know it best.

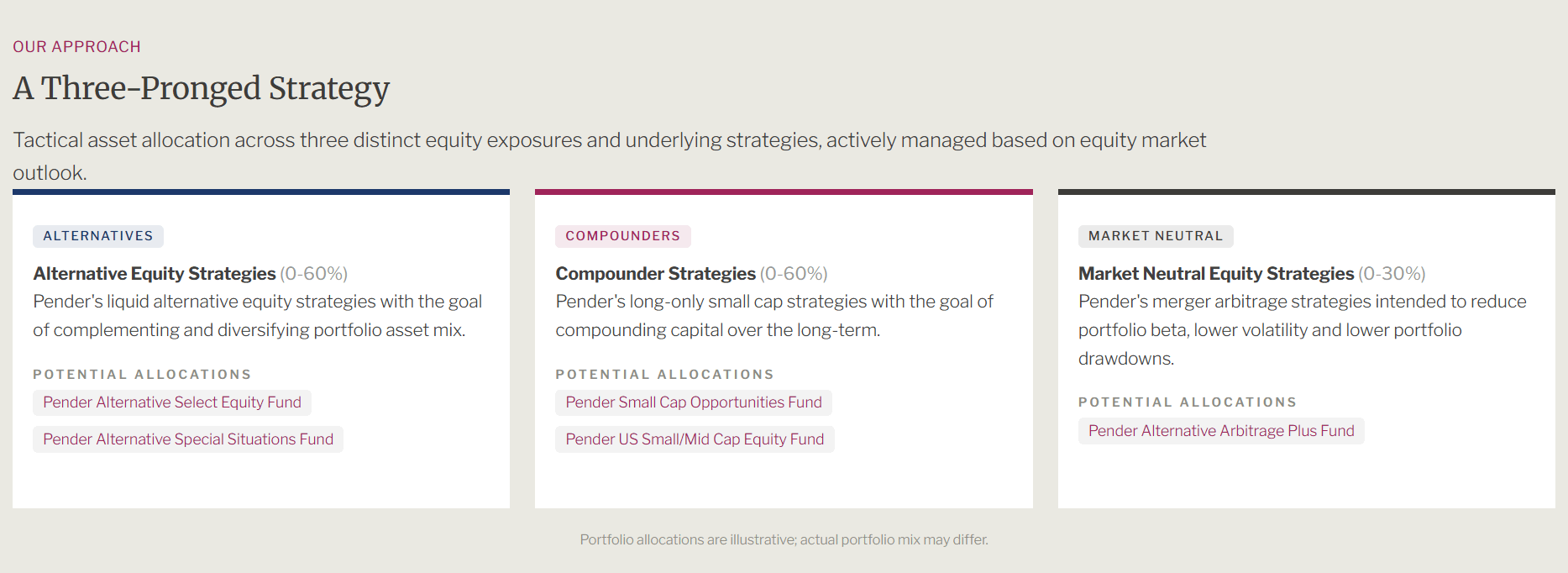

Meet the Sections: Pender’s Three-Pronged Strategy

Like any great orchestra, the Pender Alternative Multi-Strategy Growth Fund is built around distinct players, each responsible for a specific role, each capable of carrying the performance when the moment calls for it, and each most powerful when playing in concert with the others.

The Strings: The Compounders Pender Small Cap Opportunities Fund, Pender US Small/Mid Cap Equity Fund Allocation range: 0–60%

Every great orchestral performance is anchored by the strings. They carry the melody. They provide continuity. They create the foundation upon which the rest of the ensemble performs. While the brass may command attention and the percussion may punctuate key moments, it is often the strings that give the performance its character and direction.

Within the Pender Alternative Multi-Strategy Growth Fund, that role belongs to Pender’s small-cap equity strategies.

For more than two decades, Pender has built its investment culture around uncovering businesses that are overlooked, misunderstood, or simply too small for much of the investment industry to notice. While markets often focus on today’s largest companies, Pender’s equity team has consistently searched where competition is lower, inefficiencies are greater, and the opportunity to identify future compounders is often highest.

This expertise is expressed through the Pender Small Cap Opportunities Fund and the Pender US Small/Mid Cap Equity Fund, strategies dedicated to identifying businesses capable of growing their intrinsic value over years, not quarters.

Small-cap investing rewards patience, discipline, and deep fundamental research. It requires investors to look beyond short-term market narratives and focus instead on management quality, competitive advantages, capital allocation, and long-term business value creation. These are areas where the Pender equity team has spent years refining its process and developing its edge.

The result is a collection of businesses that form the melodic core of the portfolio: companies with the potential to compound capital over full market cycles while providing exposure to opportunities often unavailable in traditional large-cap benchmarks.

Just as an orchestra relies on its strings to carry the performance forward, the Growth Fund relies on Pender’s small-cap expertise as its primary engine of long-term capital appreciation.

The Brass: The Alternatives Pender Alternative Select Equity Fund | Pender Alternative Special Situations Fund Allocation range: 0–60%

If the strings carry the melody, the brass carries the conviction. Powerful, dynamic, capable of cutting through market noise with force, and equally capable of pulling back when the performance demands restraint.

Pender’s alternative equity strategies occupy this role. The Select Equity Fund brings an active, sector-rotating lens to North American equities, concentrating capital where the opportunity is richest and stepping back when it isn’t. The Special Situations Fund goes further, using long/short positioning, event-driven setups, and special situation opportunities to generate returns that traditional long-only investing often cannot access. Together these funds can profit from both sides of a trade, isolate specific catalysts such as a merger, a restructuring, a mispricing and express a view directly, without carrying the full weight of broad market exposure.

In environments where dispersion is high and single-stock differentiation matters more than macro direction, the brass section leads. It adds range and dimensionality to the portfolio that no amount of additional long-only exposure can replicate.

The Percussion: Market Neutral Pender Alternative Arbitrage Plus Fund Allocation range: 0–30%

Ask any musician what holds an orchestra together and they’ll point to the percussion section. Not the most visible. Not the most celebrated. But remove it, and the whole performance loses its footing.

Pender’s market-neutral strategy, built around merger arbitrage, is the percussion of this fund. It keeps time regardless of what equities are doing. Its returns are structurally uncorrelated to broad market direction, tied instead to the outcome of specific corporate events: announced deals and other catalysts with defined timelines and contractual payoffs. The strategy enhances those returns through the disciplined use of leverage, amplifying what is by nature a low-volatility, spread-based approach. When equity markets are volatile, when the brass is adjusting and the strings are waiting for their moment, the percussion holds the beat.

Its purpose is not to generate the fund’s highest returns. Its purpose is consistency, dampening volatility, reducing drawdowns, and ensuring the overall portfolio never loses its rhythm.

The Conductor: Active Tactical Allocation

What separates a world-class orchestra from a collection of talented soloists isn’t the quality of the individual players. It’s the conductor, the person with the full composition in front of them, reading the room, adjusting the balance in real time, knowing when to bring each section forward and when to let another carry the weight.

In the Pender Alternative Multi-Strategy Growth Fund, that role belongs to Greg Taylor, Pender’s Chief Investment Officer and a portfolio manager with over two decades of experience. Greg joined Pender specifically to lead this kind of integrated, multi-strategy mandate, bringing a track record for identifying opportunities while applying disciplined risk management at the portfolio level.

The fund’s strategy weights are not fixed. Allocations to Alternatives, Compounders, and Market Neutral strategies each carry wide bands and shift tactically based on Greg’s macro outlook, combined with the bottom-up views of the underlying portfolio managers. When the environment favors aggressive compounding, the strings are brought forward. When volatility and dispersion dominate, the brass leads. When uncertainty is the only certainty, the percussion anchors.

This is not a static portfolio dressed up as active management. It is an adaptive composition, designed to sound different depending on what the market demands, and to adapt regardless.

The Music Has Been Telling Us Something

This is not a fund built for a hypothetical future market. It was built for this one.

To understand why the timing matters, it helps to look at where markets actually stand, rather than where we hope they might be heading.

Despite years of inflationary pressure, fractured trade relationships, sanctions, geopolitical conflict, and rising deficits, markets have largely shrugged off each disruption without materially resetting valuations. It increasingly feels as though markets have become decoupled from economics. The old rules of cause and effect that we once so heavily relied on seem to have stopped applying. “This time is different” has quietly become the dominant psychology.

However, overvaluation alone rarely triggers a reset. If history is any indication, expensive can stay expensive for a very long time. The danger isn’t the price tag. The danger is what’s holding it up.

Artificial intelligence, the thesis underwriting much of today’s market concentration, contains an uncomfortable underlying tension. The productivity boom it promises requires enormous energy consumption, raising power costs for everyone. It demands capital expenditure at a scale that must ultimately be passed through to consumers. And its most visible near-term effect is the displacement of workers at a pace the economy has not had time to absorb, a slow bleed on consumer capacity that doesn’t show up in quarterly earnings until it does, suddenly and all at once.

The macro picture compounds this. Supply-side pressure is pushing inflation upward while demand-side weakness is weighing on consumption. Costs rising as spending power falls is not a soft-landing scenario. It is a compression.

Yet markets continue to look past it. The music plays on, the tempo holds, and most portfolios remain positioned as if the conductor will never reach the song’s final note.

This is precisely the environment the Pender Alternative Multi-Strategy Growth Fund was designed for. None of what we’ve described is short-term noise, and the window for traditional portfolio construction to “work again” may stay closed far longer than investors expect. Waiting for conditions to normalize carries its own risk.

The orchestra is assembled. The hall is ready. The only question is whether your portfolio is still built around a single soloist.

Pender Events + Publications

Read our latest commentaries from CIO Greg Taylor, Lead Portfolio Manager, Geoff Castle, and Portfolio Manager Aman Budhwar where they discuss the latest Fund updates. https://bit.ly/4tPT5vE

Missed the PCOF webinar? The replay is now available. Parul Garg, Associate Portfolio Manager, and Richa Nair, CIM, MBA, Director of Business Development and Investor Relations, walk through how market dislocations are widening the opportunity set in stressed and distressed credit and how disciplined credit selection can uncover asymmetric returns. “We buy in an open market, we sell in an open market, our position is market-to-market.” In the replay, you’ll hear: Where the most pronounced dislocations are emerging across public credit markets. How volatility is creating asymmetric risk/reward and high conviction opportunities. The role of active trading and fundamental credit work in generating alpha. Watch the full replay: https://bit.ly/4vpT8Ox

New Podcast - In this episode, Aman Budhwar, Portfolio Manager of the Pender US Small Mid/Cap Equity Fund spoke with Laura Baker, Associate Client Portfolio Manager to discuss several key themes of the Fund. Topics included: How active management can capitalize on overlooked and misunderstood businesses. The valuation disconnect between mega caps and the small/mid-cap universe. “The key objective as most fund managers would say is to outperform the market over long periods of time with the protection on the downside. We don’t just say that as a statement, we actually live by that.”

Introducing the Pender Alternative Multi-Strategy Growth Fund - a new strategy that goes beyond traditional long-only equity markets targeting the best risk reward. Leveraging Pender’s small cap compounders, our alternative equity and market neutral strategies, the Fund aims to deliver differentiated growth through diversified equity return streams with minimized volatility. Learn more: https://bit.ly/4ucLhTY

Market Snacks

SpaceX starts trading on the Nasdaq today in what’s priced to be the largest IPO ever. The rocket launch/internet satellite/social media/AI chatbot company set its share price at $135 and expects to raise $75 billion in its public debut, after which its estimated value will land at roughly $1.77 trillion. SpaceX could immediately be worth more than Tesla, as well as Meta and Berkshire Hathaway. The hottest IPO ever has huge demand. BlackRock is reportedly on the books for at least $5 billion worth of shares, while sovereign wealth funds including Saudi Arabia’s Public Investment Fund have placed orders for stakes of $1 billion or more. Altogether, about 1,000 institutional investors want a piece of the IPO.

Blackstone is in discussions with Canada’s H&R REIT about a potential acquisition, according to people with knowledge of the matter. That follows takeover negotiations last year involving H&R, Blackstone, TPG Inc. and Crestpoint Real Estate Investments Ltd. falling apart, said the people, asking not to be identified because the discussions are private. H&R has spent several years moving its portfolio away from struggling office and retail holdings and increasing its exposure to apartment and industrial assets in the US and Canada.

Toronto-based startup Beacon Software raised US$225 million at a $1.4 billion valuation. Beacon is what’s called an AI-rollup company, which means it acquires software firms, introduces AI into their operations, and then holds onto them indefinitely as their value grows.

Koho just became Canada’s newest unicorn. The fintech raised $130 million in its latest funding round, valuing the company at ~$1.3 billion. Shopify co-founder (and professional racecar driver) Tobi Lütke was one of the investors to join Koho’s cap table in the funding round. The company is in the final stage of getting a federal banking licence, which Koho’s CEO says will allow it to compete directly with the Big Six banks. (BetaKit)

Macro Morning

ECB raises interest rates for first time in nearly three years. Europe’s central bank, one of the most important in the world, hiked rates from 2% to 2.25% yesterday, becoming the first major central bank to do so since inflation accelerated as a result of the war in Iran. The US Federal Reserve, however, is expected to keep rates steady when it meets next week. While President Trump has frequently called on the Fed to cut rates, observers say that the central bank may be more likely to raise them to combat rising energy prices.

Ottawa unveils $3.2 billion food security program. The new federal food strategy includes a $1 billion investment over the next decade to build food terminals and hubs, which sell produce to independent grocers at prices that allow them to compete with big chains. The overarching goal of the plan is to increase grocery competition and produce more food in Canada. The country currently imports half of its food from the U.S. and gets between 72% and 88% of its fresh produce from other countries. (CBC News)

Canada Post will end home delivery for 485,000 more houses across the country, which will move to community mailboxes starting next year.

The Gordie Howe International Bridge, named for the legendary Canadian Detroit Red Wings player, was due to have its opening celebrated today. But the ribbon-cutting was canceled after the US and Canada were apparently unable to resolve issues raised by President Donald Trump.

The Supreme Court ruled that shareholders can’t sue investment funds under the 1940 Investment Company Act.

Technology Today

Scientists are refining the design of NASA’s Habitable Worlds Observatory to maximise its ability to detect signs of life on Earth-like exoplanets.

Nearly 40% of data center projects in development this year are at risk of facing significant delays, according to an April Financial Times analysis of data provided by satellite group SynMax. Lack of access to sufficient power was cited as a leading reason for the delays, as well as labor and other supply shortages. An even more recent analysis by Goldman Sachs published in May found that as little as 50% of data center capacity scheduled to come online in the next two years is on track to do so on time amid delays and shortages.

Canada’s introduces bill to ban social media for kids under age 16, following the lead of Australia, who banned it earlier this year.

AI of the Tiger

OpenAI is reportedly considering major price cuts as competition with Anthropic gets sharper. The company is reportedly looking at lowering token prices as a reminder, tokens are what AI firms use to charge customers for using their models. OpenAI CEO Sam Altman recently said costs had become “a huge issue,” adding that the company wants to help users get more value for less money.

DoorDash is launching a new AI chatbot that lets users order food, groceries and restaurant bookings using text prompts, photos or recipe links. The feature, called Ask DoorDash, is designed for people who know they’re hungry but do not have the emotional strength to scroll through all the menus. Instead users can describe what they want, upload a grocery list, share a recipe, or ask for a table at a specific time. DoorDash is joining a wider AI push in food delivery and shopping, with Uber Eats and Instacart also adding AI-powered assistants

Jeff Bezos opened up about a new artificial intelligence project. Prometheus, the startup where he’s co-CEO alongside former Google executive Vik Bajaj, said it raised $12 billion at a $41 billion valuation from investors including the Amazon co-founder himself. Bezos told media outlets that Prometheus, which launched in November and has no ties to Amazon or his space firm Blue Origin, is developing what it calls an “artificial general engineer,” or an AI to work on the engineering side of physical products. The details are still mum, but Bezos suggested Prometheus AI models could develop and refine prototypes for everything from jet engines to buildings to consumer electronics to medical devices. This, Bezos said, would reduce the time it takes for human engineers to complete complex projects.

Red Lobster CEO Damola Adamolekun said this week he wants to make the chain “the most AI-forward restaurant company that exists,” with plans for AI-generated performance reports, sales forecasting, and employee scheduling. No word yet on whether the AI plans to bring back Endless Shrimp—but since that promotion helped push the company into bankruptcy… I’d think maybe not?

Defense Docket

A court has sentenced former president Yoon Suk Yeol to 30 years for sending drones into North Korea in an attempt to provoke a Pyongyang reaction and aid his failed martial law bid (for which he’s already serving a life sentence). (Korea Times)

The Taiwanese coast guard has vowed to expel China-based vessels that recently “harassed” foreign merchant ships, while the military has conducted its first live-fire test of US-supplied HIMARS rockets along its China-facing shore. (TaiwanNews)

Trump canceled strikes on Iran, citing progress on deal. Thursday began with the president posting to Truth Social that the US would be striking Iran “VERY HARD TONIGHT,” but in the afternoon, he made another post saying the two countries were close to a deal, the time and place of the signing would be announced shortly, and the strikes were canceled. A spokesman for the Iranian Foreign Affairs Ministry told the Tasnim news agency that no agreement had been finalized. Last night, a US official said that the military shot down two Iranian one-way drones that were targeting commercial ships transiting the Strait of Hormuz

Trump names former SEC chairman as permanent spy chief. About a week after picking controversial housing official Bill Pulte to replace Tulsi Gabbard as acting director of national intelligence (DNI), President Trump said he was nominating Jay Clayton, the current US attorney for the Southern District of New York and the former head of the SEC, to serve in the role permanently. The president had been under pressure to nominate someone else after his appointment of Pulte—who has no intelligence credentials—was met with bipartisan criticism. Earlier on Thursday, the House voted to reject the reauthorization of a critical surveillance tool, FISA, with many Democrats saying they wouldn’t vote for it as long as Pulte was serving as DNI. The program is set to expire today if it’s not extended

Crypto Corner

Following its recent price tumble, about 50% of all circulating bitcoin supply is now trading at a loss for the first time since 2022.

Bernstein calls FIFA World Cup a ‘watershed moment’ for prediction markets, projects $5-10B consumer volume surge. The firm projects that the tournament will fuel a $5 billion to $10 billion surge in consumer volume. Major platforms like DraftKings, Robinhood, and Coinbase are aggressively positioning their products to capture this massive sports betting handle. [Read more]

Citigroup to offer tokenized shares of private companies for wealthy and institutional clients. This rollout extends the bank’s push into tokenization, a sector it projects could hit $4 trillion by 2030. [Read more]

Energy Transition Today

The U.S. got more electricity from solar than it did from coal in May. The figure for May denotes the fourth-lowest monthly share that coal has ever seen, only slightly greater than the all-time low of 11.7% observed for April. From 1984 until 2010, coal was America’s largest source of energy. However, as the fossil fuel continues to fall out of favor, that share has been almost cut in half in the last five years alone

Brian Martucci has a great story about the potential for farmers to use wind power to produce cheaper, more reliable fertilizer

As election season heats up and energy affordability concerns mount, some Democrats are questioning the wisdom of ambitious climate and decarbonization policies and showing more openness to new fossil-fuel projects. (New York Times)

New York’s Public Service Commission is now formally seeking input on the best way to build 4 gigawatts of new nuclear power, as directed by Gov. Hochul. (E&E News)

The U.S. is expected to generate about 19% more solar power this summer than it did during the season last year, while coal generation is likely to slip by 2%, according to the U.S. Energy Information Administration. (Utility Dive)

The Dig

More tungsten market consolidation on the cards in wake of China’s export ban - More consolidation is afoot in the tungsten industry as Western users scramble to secure supply from existing assets, experts told Platts, part of S&P Global Energy.

Venezuela deployed troops against illegal groups controlling gold deposits in the country’s Bolivar state, Reuters reported, citing local residents and human rights activists.

Gold may be struggling to live up to its safe-haven reputation, but there’s another metal that’s having a much better year. Average tin prices have doubled since 2003 to about $49,000 per tonne, driven by demand for solder, the tin-first alloy used to connect components on circuit boards in AI servers, semiconductors, and other computing equipment. Supply constraints have amplified the rally, with nearly three-quarters of global production concentrated in just three countries. Tin options volumes more than doubled year over year in the first four months of 2026, while trading activity in Shanghai has surged. The metal has even joined silver and copper as one of the market’s favorite “internet metals,” as traders bet that AI-driven demand for tin is only getting started.

The Picks List

The World Cup 2026 is officially underway. For the 45% of Americans who have “no interest at all” in the international tournament, don’t worry — there’s only 102 matches left

America’s soccer problem - Americans’ relationship with soccer doesn’t quite make sense. They like to play it — by some accounts it’s the third most popular sport in the U.S. — but they don’t really care about it on a professional level, at least not when it’s played in their own country. Instead, Americans are passionate about European football. Oddly, it’s not for lack of star talent. Americans are actually very good at exporting top tier players, writes Gabriel Debenedetti in Bloomberg Weekend. Nine of the US Men’s National Soccer Team’s starting lineup plays soccer in Europe, often for elite teams. But the home front hasn’t caught up.

There is growing rumors online that Shakira has been replaced with a body double for the World Cup Opening Ceremony

A chess scandal stalemate

The first ever leather bag made from T-Rex cells is being auctioned off.

JM Smucker says it sold $1 billion worth of Uncrustables in FY2026. Over the last two decades, annual sales of Uncrustables have skyrocketed, rising 162% from a reported ~$76 million in 2006 to ~$199 million in 2016... then jumping another 403% across the next 10 years to hit a whopping $1 billion in the last fiscal year. Since the crimped discs have attracted support from the likes of Travis Kelce and Lil Yachty — and Smucker completed its 900,000-square-foot megafactory, dedicated solely to manufacturing Uncrustables, in November 2024

Quebec became the first province to ban the sale of energy drinks to people under 16, passing a law in the National Assembly yesterday that will come into effect in six months.

The Breakroom

Check out a ESPN ranking of the 105 jerseys you may see on display at the 2026 World Cup… if you’re in the 13% of Americans who say they’re definitely tuning in.

£64.2 million. Prize money at Wimbledon this year, a record high for the tennis tournament and a 20% increase from last year. The boost comes as players have threatened to boycott the tour until they get a greater share of the revenue from tournaments. Only ~15% of Wimbledon’s total revenue is allocated to prize money.

In ancient Greece, killing a dolphin could get you killed. Dolphins were sacred to Apollo and Poseidon, so harming one was treated like a religious crime on the level of killing a person. My only question is, why was this protocol ended???

An English gentleman is in hot water after he grabbed a seagull out of the air and punched it to death after it stole his pastry. Um…

Ryanair is being investigated over charges that require parents to pay extra to sit with their children on flights.

Noel Gallagher has criticised plans for the World Cup’s first-ever halftime show, arguing football doesn’t need a concert spectacle.

Disclosure Day debuts today in theaters, a film about UFOs and aliens that Spielberg calls ‘closer to fact than fiction.

Please read important disclosures at www.penderfund.com/disclaimer.

Standard performance data for Pender Funds can be found at www.penderfund.com/solutions/